Market Snapshot: Flipping the Script on Market Concentration

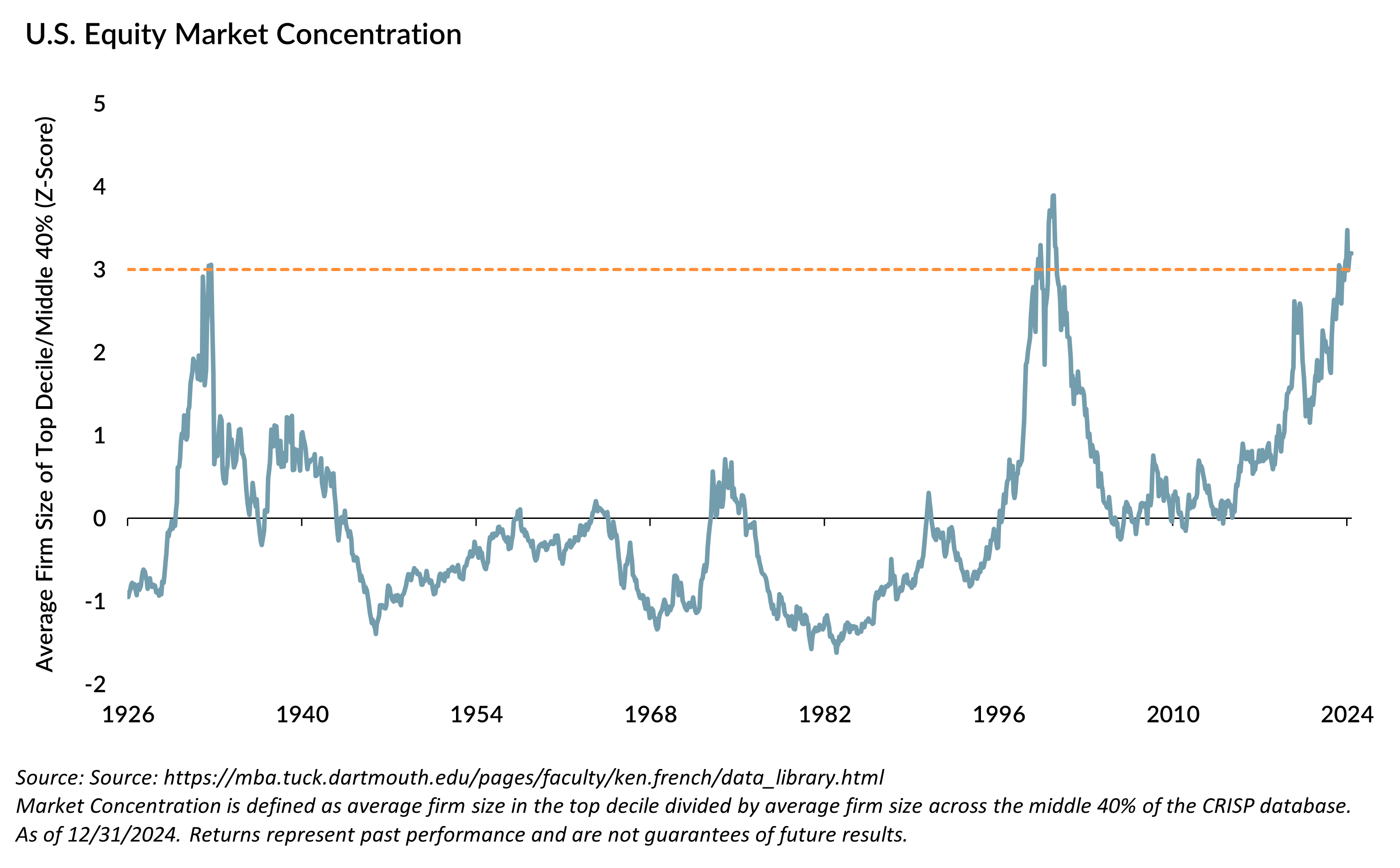

U.S. large cap passive indices remain at historically high market concentration levels, which we continue to see as a risk to investors with sizable allocations to U.S. large cap passive strategies. As a representation of the current extreme market concentration, the graph compares the average firm size in the top decile divided by average firm size across the middle 40% of the CRISP database. Current levels are three standard deviations above normal, something only experienced during the 1920s and the dot.com days of the 1990s. In the previous periods with observations above three standard deviations, the middle 40% had 3-year cumulative returns 54.4% greater than the top 10% market cap stocks (49.9% vs -4.5%, respectively) and 5-year cumulative returns 71% greater (69.3% vs. -1,8%, respectively).

An alternative argument to concentration is the underperformance of the S&P 500 cap weighted versus equal weighted index. Over the past 66 years, the S&P 500 Equal-Weight Index has outperformed the S&P 500 cap-weighted index by 2.7% on an annualized basis. Currently, the equal-weighted index is 37% below the longer-term trend line of relative performance to the cap-weighted index. A return to the trend line would be an average 9.6% outperformance of the equal-weighted index to the cap-weighted index over the next five years. This would be in line with what the markets experienced following the 1963 and 1999 periods of similar deviations from the equal-weighted versus cap-weighted relative returns trend line.1

Hindsight bias is the tendency for people to assume past events are more predictable than they really were. While we continue to believe that the current market concentration of U.S. large cap passive indices with the Magnificent Seven will eventually crack and the market will experience strong returns across more than just seven stocks, as students of behavioral finance, we know that we cannot predict when that will happen with any true certainty. We also know its near impossible for anyone else to predict that as well. We do, however, believe that managing risk through diversification can lead to better risk-adjusted returns to help meet long-term investment objectives. Ultimately, we may be early or perfectly spot on to the normalization of market concentration, but regardless, we continue to believe diversifying some U.S. large cap passive allocation to an actively managed strategy with a focus on diversification and compelling valuation is an attractive risk/reward for investors.

1After the 1963 drawdown the equal-weight outperformed by 12.3% (annualized) over the next five years. After the 1999 drawdown the equal-weight outperformed by 10.4% (annualized) over the next five years.

Sources: Glenmede Investment Management LP and https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

Market Concentration is defined as average firm size in the top decile divided by average firm size across the middle 40% of the CRISP database.

All data as of 12/31/2024, unless otherwise noted. This represents past performance which is not indicative of future results. Securities mentioned are for informational purposes only and do not represent a recommendation or an offer to buy, hold or sell any securities, or all of the securities held in client portfolios. As with all investments, loss is possible. See Additional Disclosures at the end of this document.

Views expressed include opinions of the portfolio managers as of February 6, 2024, based on the facts then available to them. All facts are gathered in good faith from public sources, but accuracy is not guaranteed. Nothing herein is intended as a recommendation of any security, sector or product. This is not intended as a solicitation for any service or product. All investment has risk, including risk of loss. Intended for professional and adviser use.