Market Snapshot: Earnings Surprises—Mag 7 Approaching Lag 7

Positive earnings surprises for the Magnificent Seven have been more in line with the broader S&P 500 index this year relative to last year, suggesting that expectations are high and exceeding expectations is becoming more difficult. In 2023 the Magnificent Seven stocks saw, on average, a 13.5% positive earnings surprises compared to the S&P 500 average of 9.4%, while in 2024 earning surprises were similar for both the Magnificent Seven and S&P 500 Index (7.0% versus 6.5%, respectively).

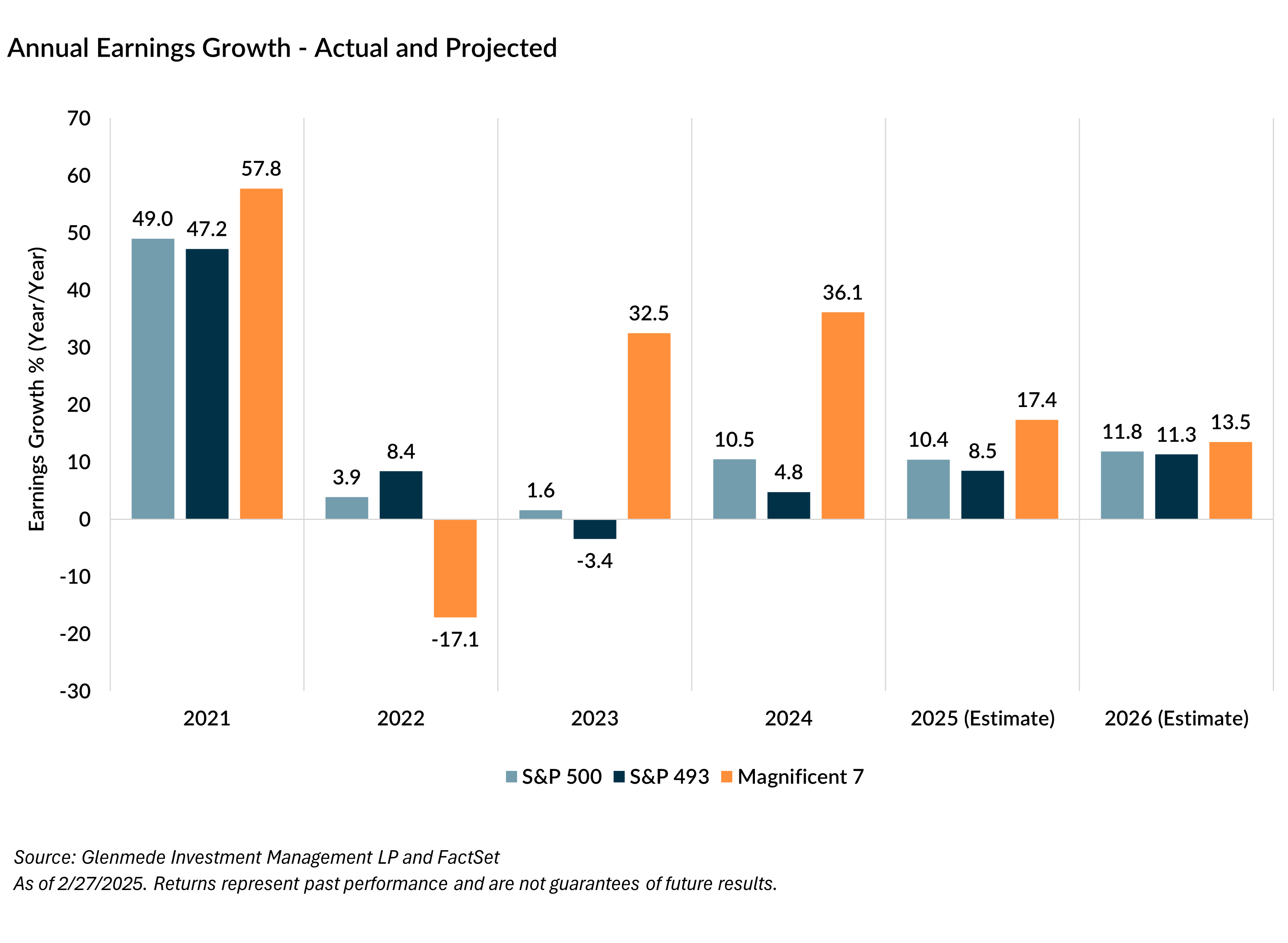

Earnings growth for the Magnificent Seven had more upside volatility in the post-Covid years (with the exception of 2022) at multiples of the broader index and remaining 493 stocks, as shown in the chart. Projected estimates for 2025 and 2026 show a potential normalization of the growth premium between the Magnificent Seven and the rest of the index. During the four years from December 31, 2020 to December 31, 2024, an equal-weighted basket of the Magnificent Seven outperformed the S&P 500 Equal Weight Index by more than three-fold (Magnificent Seven had an annualized average return of 30.1% versus S&P 500 Equal-Weight of 10.2%).

As of February month-end, the Magnificent Seven was trading at a 12-month forward price/earnings ratio of 27.6x, which compares to the rest of the S&P 500 index at 19.9x. With expectations for earnings growth of the Magnificent Seven to potentially be more in line with the rest of the index in the next year, according to FactSet estimates, and earnings surprises to normalize, should the valuation disparity also be normalizing? Exposure to the Magnificent Seven and any potential upside surprises can be achieved through large cap passive strategies. Investors looking to de-risk some of the exposure to these companies, however, may continue to favor some allocation to an actively managed large cap strategy with a focus on diversification and attractive valuation.

Views expressed include opinions of the portfolio managers as of March 13, 2025, based on the facts then available to them. All facts are gathered in good faith from public sources, but accuracy is not guaranteed. Nothing herein is intended as a recommendation of any security, sector or product. This is not intended as a solicitation for any service or product. All investment has risk, including risk of loss. Intended for professional and adviser use.